Bond yields rocketed higher on Wednesday as oil prices surged and central banks signalled a growing willingness to tighten if inflation broadens.

Markets are now aggressively repricing policy expectations—most notably in Canada, where rate cuts have vanished without a forwarding address, and a summer hike is back in play.

Yield Movers

Wednesday’s news flow drove yields:

- Higher: The BoC maintained its 2.25% overnight rate for the fourth straight meeting, right on cue. The central bank sees “little evidence” of high oil prices driving persistent inflation, but that’s only because oil shocks can take multiple months to filter through to core prices. Governor Macklem warned that if price increases become more widespread, “there may be a need for consecutive increases in the policy rate.” MLN provided the rate context here.

- Higher: As unanimously predicted, the Fed left its policy target at 3.50% to 3.75%, though the decision was the most divided in decades. Three policymakers objected to the “inclusion of an easing bias in the statement at this time.” MLN unpacked that news here.

- Higher: WTI prices ripped higher yet again, with spot WTI crude up 6.8% to $110.47 on deadlocked U.S.-Iran negotiations. Crude looks destined for multi-year highs, barring divine intervention. Oil has rallied almost nonstop since April 17, when Trump said the Strait of Hormuz was “fully open and ready for business and full passage,” a statement that aged about as well as you’d expect.

News also broke that Trump met with top oil firms about the possibility that the blockade could last months. “They discussed the steps President Trump has taken to alleviate global oil markets and steps we could take to continue the current blockade for months if needed and minimize impact on American consumers,” said the White House.“Oil is driving the repricing in the rates curve. The market is highly concerned that the U.S. is committed to a long-term blockade.”

–Adam Button | chief currency analyst, investingLive

- Higher: U.S. core capital goods orders increased 3.3% in March, shattering forecasts (est. +0.5%, prior +0.7%). The AI investment boom continues to bolster business spending on equipment and infrastructure.

“The stunning degree of strength during a month when firms would have had valid reason to be cautious attests to the substantial energy in business investment that was bottled up last year due to policy-related uncertainty,” noted Stephen Stanley, Santander U.S. Capital Markets.

Curve Chronicles

Today’s mortgage headline is the abrupt shift in policy expectations for the Bank of Canada.

OIS traders have completely erased rate-cut odds and are now eyeing a 50% chance of a July hike. All markets needed was a reminder from the BoC that a tightening bias is possible.

Expect the outlook to swing wildly over the coming weeks as markets digest Trump’s war moves and as energy costs work their way through the system.

For now, though, the direction is clear: a surging CPI is bullish for the mortgage rate outlook, and that’s exactly the kind of clarity borrowers were hoping to avoid.

Quote Board

The 5-year yield is opening 2 ticks lower this morning at 3.24%.

Funding cost indicators closed strongly higher on Wednesday:

- Canadian 5-year bond yield: +12 bps

- U.S. 5-year bond yield: +9 bps

- 5-year CMB: +12 bps

- 10-year CMB: +10 bps

- 4-year swap: +14 bps

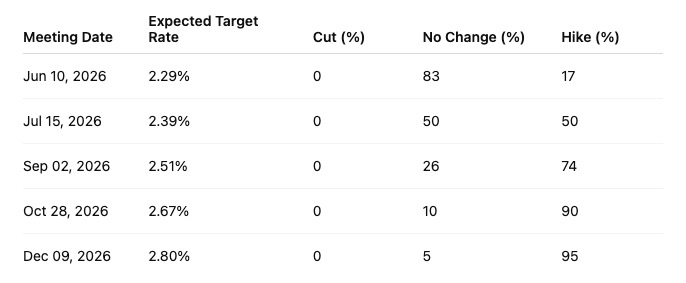

Policy Probabilities

Here’s how markets are pricing in future policy this morning:

- For the Bank of Canada meeting on June 10:

- 25 bps hike: 18% chance

- No change: 82% chance

- For the Federal Reserve meeting on June 17:

- 25 bps cut: 4% chance

- No change: 96% chance

Written by the team at MLN